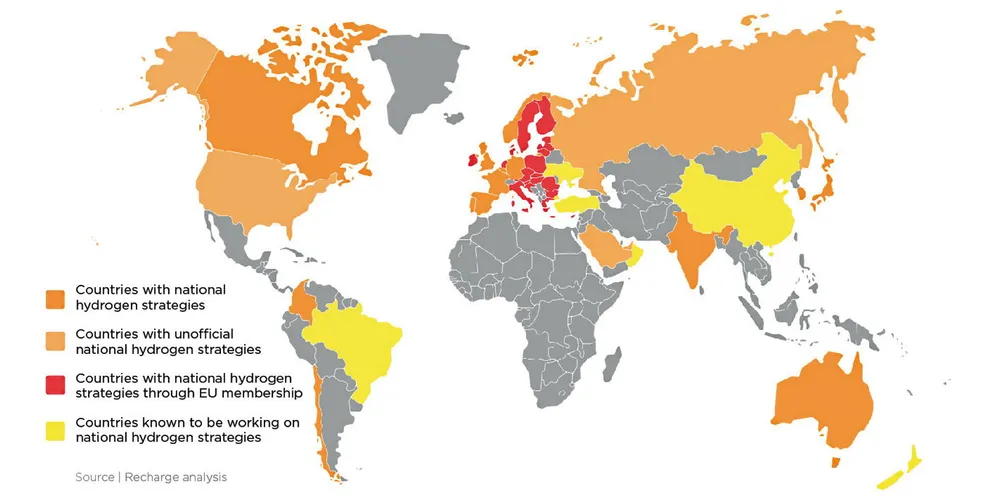

Hydrogen now firmly at the heart of the global race to net zero — for better or worse

New policy announcements by the US, EU, UK, India and Russia show that major economies are getting serious about H2, but are they getting it right? asks Leigh Collins