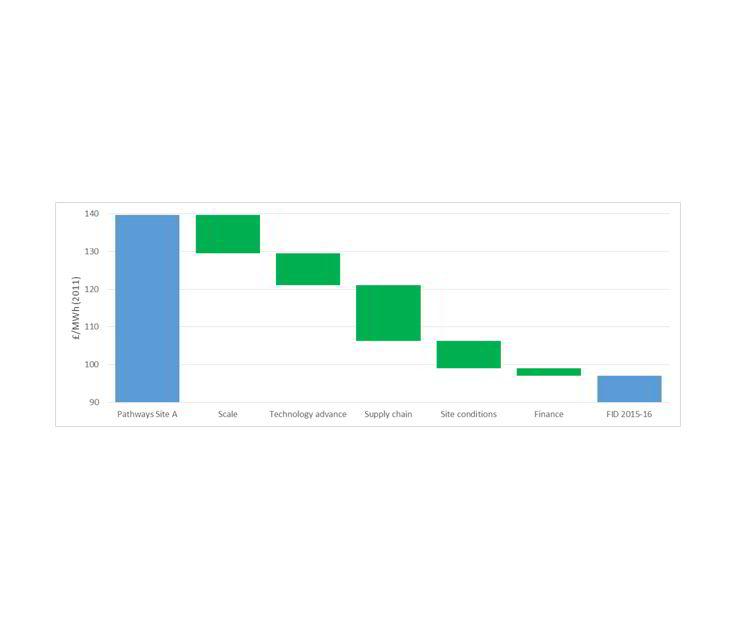

A recent offshore wind study came to a striking conclusion — that the target of achieving a levelised cost of energy (LCoE) of £100/MWh by 2020 had been achieved four years ahead of schedule.

The LCoE for UK offshore wind has fallen by 32% — from £142/MWh in 2011-12 (for projects taking a final investment decision [FID]) to £97 ($122/€113) in 2015-16, according to the Cost Reduction Monitoring Framework 2016 report (CRMF), produced by ORE Catapult for the Offshore Wind Programme Board.

And